Are there any requirement for withholding taxes on payments in Nepal?

The withholding tax (WHT) provisions in Nepal is quite complicated because it also covers normal business payments such as service fees or contractual payments by a resident person to a resident person. WHT is commonly called TDS or Tax Deduction at Source.

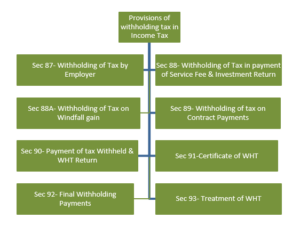

WHT requirements is depicted picture below.

The payer (withholding agent) is required to withhold taxes (deduct TDS) on certain payments prescribed by the Act as

per the prescribed rates. The taxes that are withheld are Withholding Taxes, also called TDS (tax deduction at source) in

common parlance. The person who is responsible to withhold tax is Withholding agent and the person from the payment

made to whom the tax is withheld is Withholdee. The government receives withholding tax, and the withholdee receives

payment amount after such withholding of taxes.

Taxes should be withheld at the time of payment to the recipient. But in case the taxpayer recognizes expenses under accrual basis of accounting before the actual payment is made, the withholding tax should be deducted at the time of making accounting entry in the books.

Practical issues arise due to:

- Difference in interpretation- if the payment is subject to TDS or not? Or at what rate?

- Withholder not depositing TDS within time, and Withholdee made responsible.

- IRD imposing tax after years to payers which the payer cannot recover from payee.

- Increased cost to international businesses due to uncertainties in explanation

Withholding taxes are discussed further in other sections of this site.